Methodology

Weighted Price Index

The ASE Market Capitalization Weighted Index is presently made up of the most liquid and largest 100 companies from the First and Second Markets. The company's weight in the index is determined by its relative percentage of the aggregate market capitalization of the 100 companies. A base value of 100 points on December 31st, 1991 was stipulated for the ASE weighted index. The stocks included in the index represent around 90% of the aggregate market capitalization of the listed companies in the regular market. The ASE weighted price index is supplemented by sub-indices for the four sectors: Banking and Finance Companies, Insurance, Services and Industrial sector. The base was changed to 1000 as of January 1st, 2004.

The ASE weighted index provides a comprehensive measure of the market trend to investors or institutions who may be interested in general market price movement.

Methodology:

The index is calculated using the Paasche method.

The general formula for the index (t ) is:

At t=1,

Index = 1000

B1 = M1, or market capitalization = base value of the index

At t>1,

Index (t) = (Mt/Bt)*1000

Bt = Bt-1*(Mt/Mad)

Mad = Mt - It - Nt + Qt-1

Where,

t: time period

index (t) : index at time t

Bt: base value of index

Mt: market capitalization of constituents at time t ( the sum of the market capitalization of all stocks included in the index)

Mad: adjusted market capitalization at time t. The adjustments are done for new issues of shares, and the addition or deletion of constituents

It: market capitalization of new shares issued by a company included in the index and listed at time t

Nt: market capitalization of the company added to the index at time t

Qt-1: market capitalization of the company at time (t-1) which deleted of the index at time t

The base value Bt is an adjusted base (market capitalization) which is not the real market capitalization at the base period.

No adjustment is made, however, in case of a stock split, bonus shares (stock dividend) and a decrease in paid-in capital, since such corporate actions do not affect the current market capitalization. Thus, adjustments are done for any changes in index sample or any corporate action affecting the market capitalization of index stocks. This can be achieved by using the adjustment factor Mad.

Without any adjustments, such changes would cause sudden and sharp movements of the index value which would not reflect the market's actual behavior.

Free Float Index

One of the features of this index is giving better reflection for the changes of stocks prices in the market by not being biased to the companies that have large market capitalization, thus, providing diversification in the index sample by giving better chances to small and medium companies to reflect the index.

This index is calculated using the market value of the free float shares of the companies and not the total number of listed shares of each company.

The ASE calculates the following indices based on the free float shares:

- General index ASEGI: includes the most active companies at the ASE and the highest in terms of market capitalization. (Base year: 1999=1000)

- ASE20: includes 20 listed companies that are most active and the highest in terms of market capitalization, which are the leading companies in the ASE. The sample of this index was selected from the general index sample ASE100. (Base year: 2014 = 1000)

- Markets indices: These include the first market index and the second market index. (Base year: 2012 = 1000)

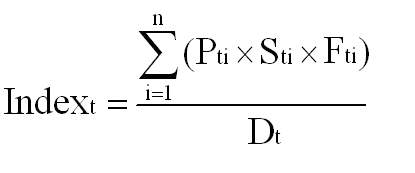

This formula is used to calculate the above indices:

Where:

Pti: closing price of the company i on day ( t )

Sti: number of listed shares of the company i on day ( t )

Fti: the factor of the company i on day ( t )

Dt: divisor index on day ( t )

Factor (F) is a number between zero and one. The calculation of this factor depends on the company free-float ratio that represents the total listed shares minus the shares owned by the board of directors, investors who owned more than 5% and any government ownership. The value of this factor is changed quarterly by the ASE at the time of the index re-balancing.

4. Total return index ASETR: It is a weighted index based on the market capitalization for the free float shares available for trading which measures the change in the share prices of the companies included in the index sample in addition to the cash dividends of these companies assuming that these dividends were reinvested in the shares of the companies in the index sample.This index is characterized by helping investors measure the total return on their investments in the ASE, which includes not only the price change of the shares, but also cash dividends.

This formula is used to calculate the total return index:

Total Return Index Value =Previous Day index level ∗ Market Cap

Previous Day Market Cap - Mass Dividend

Unweighted Price Index

In the ASE Unweighted Index, all stocks carry equal weight. There is no consideration of the market capitalization, and the price level does not have an impact because the index formula deals with percentage changes only. Such an index can be used by an investor who invests equal amounts of money in each stock in his/her portfolio. This index has been introduced in 1980 with the opening session of January 1st, 1980 set at 100 points. In 1992, the ASE introduced some modifications to the index, of which was the changing of the base period to December 31st, 1991. The unweighted index is supplemented by sub-indices for the four sectors: Banking and Finance Companies, Insurance, Services, and Industrial. The base was changed to 1000 as of January 1st, 2004.

Methodology:

The general and sectoral indices are calculated using the following method:

Index (t) = Exp (Ln(10)*S)*1000

Where,

S = ( Log (Pti / Poi) ) / n

n: sample size

t: time period

Exp: Exponential function to the base (e)

Ln: Natural Logarithm to the base (e)

Log: Logarithm to the base (10)

Index (t) : Index value at time t

Pti: Closing price of the ith stock at time t

Poi: Closing price of the ith stock at the base period

The unweighted index uses the logarithmic function to smooth the extreme prices fluctuations. The above formula is similar to using the geometric average of the percent changes in the stock prices of the index constituents.

Adjustments are made to the prices when the stock splits or stock dividends occur. Additions or deletions of stocks can be adjusted by computing an adjustment factor C which is equal to the value of the index after the addition or deletion takes place divided by the value of the index before. After that, the index will be multiplied by the factor C, i.e.

C = ( Index after the addition or deletion)/(Index before the addition or deletion)

Index (t) = C*Exp (Ln(10)*S)*1000

Note that the factor C will be used on the day of the adjustment and thereafter. The adjustment factor C is calculated in such a way that, at constant stock prices, the value of the index before and after the addition or deletion remains exactly the same.

Noting that the ASE discontinued calculating this index since June 2021.